:format(jpg)/prod01/channel_3/assets/media-centre/Danger-in-numbers-banner-Paul-Mazzola.jpg)

There's danger in the numbers

Can the Reserve Bank of Australia put the inflation genie back in the bottle?

May 5, 2024

As the Reserve Bank of Australia attempts to curb inflation, now could be the perfect time for the government to step in and lend a hand, writes Dr Paul Mazzola.

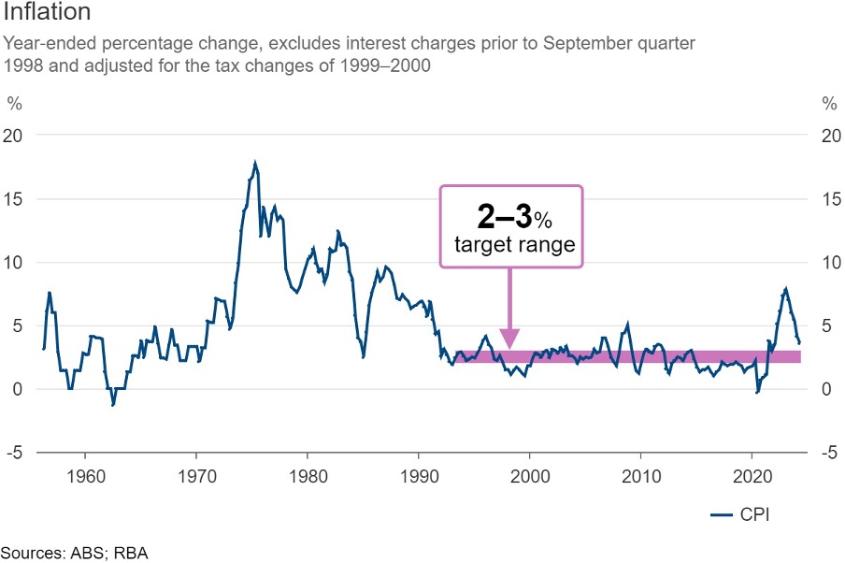

Tuesday’s cash rate announcement is particularly important in the Reserve Bank of Australia's (RBA) attempt to put the inflation genie back in its bottle. The annualised inflation rate to 31 March 2024 has declined from 4.1 per cent to 3.6 per cent. This marks the fifth consecutive quarter of lower annual inflation since the peak of 7.8 per cent in the December 2022 quarter.

Although the trend is welcome, economists are concerned it is occurring too slowly to return inflation to the RBA target range of 2 to 3 per cent by year end. In fact, some leading economists are proposing two to three more cash rate increases before the end of the year – just to make sure we bludgeon the inflation beast before it gets away from us. But is this the best course of action now?

The aim of increasing interest rates is to reduce aggregate demand in the economy, thereby reducing pressure on consumer prices - otherwise known as ‘contractionary’ or ‘tightening’ monetary policy. There’s always the danger however that if tightening is overdone, we risk dragging the economy to a halt and plunging the country into recession.

Unrestrained inflation is also dangerous as it manifests into unreasonable inflationary expectations across the economy. This is a sociological phenomenon whereby individuals and organisations are driven by the need to simply keep up with the perception of a never-ending rise in the cost of living.

The danger lies in the potential for a ‘wages push’ which induces manufacturers and service providers to routinely reprice their goods and services upwards leading to an inflationary spiral. Something we last experienced in the 1970s and 1980s (see the chart below).

The Data

The RBA prides itself on evidence-based decision-making. It has been reasonably successful in constricting inflation, but not without considerable pain. The cash rate has risen by 4.25 per cent between May 2022 and December 2023 - and the job isn’t finished yet. A reduction in spending on goods and services has not been uniform. Specifically spending on services has become ‘sticky’, with some items in the CPI basket moving backwards. We’re at a delicate stage in the process. Not an enviable position for the RBA board. The trick is in a detailed analysis of the data and an understanding of the limitations of monetary policy.

The latest data shows that the principal driver behind the March quarterly 2024 inflation rate is services inflation, not goods inflation. These include rents (+2.1 per cent for the quarter), secondary education (+6.1 per cent), tertiary education (+6.5 per cent) and medical and hospital services (+2.3 per cent). Other major services components under pressure include insurance and financial services.

It is arguable whether an increase in the cash rate would impact greatly on most of these necessary (demand inelastic) expense items. Would you pull your child out of school, go without medical attention, or move out of your rental accommodation? In fact, evidence suggests that the recent rise in rents have been caused by the historically high level of immigration earlier this year.

Generally, there is a lag between interest rate rises and rental increases, with property investors trying to maintain rental yields at the time of lease renewals. However, a simple and more targeted solution to the current round of escalating rents could include a pullback in immigration, which would also assist in dampening aggregate demand. A longer-term solution should entail an increase in housing stock.

Services inflation also relies heavily on the degree of slack in the labour market and level of productivity. There are signs of an increase in the unemployment rate later this year, so we shouldn’t expect services inflation to come down until the subsequent softening of labour costs. The only saviour for an immediate reduction in services inflation rests on an imminent lift in productivity gains – a bit optimistic, I think. So, any interest rate increase this month is expected to have a relatively benign effect on services inflation.

Monetary policy – a blunt instrument

It is generally understood that about a third of Australians have a mortgage, a third own their homes outright and another third are renters. As the principal focus of monetary policy are mortgage holders, the RBA’s cash rate tightening is unfairly directly targeting one third of the Australian population, with indirect and time lagged impact on another third - renters. According to the IMF, Australia already has one of the highest levels of mortgage rates in the world. So, it seems that the monetary policy burden is being principally carried by the battlers in our economy.

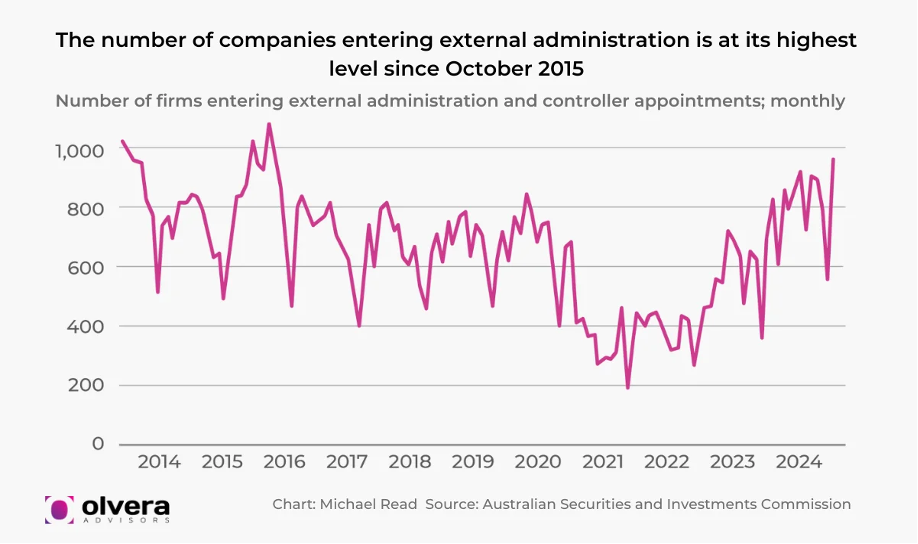

Moreover, many businesses, like mortgage holders carry some form of debt and are struggling with the same services input costs. Data from the Australian Securities and Investment Commission shows that insolvencies are up 40 per cent in the year to February 2024 - the highest level in a decade. This is a problem because as the biggest employer in Australia (accounting for over 42 per cent of the private sector), small business is crucial to our economy.

Any thoughts of a rate rise this month should be avoided. With only one third of Australians having a mortgage (those directly impacted by rate rises), goods inflation already down somewhat and services inflation proving to be sticky, any expectation that a rate rise will materially impact aggregate demand soon is wishful thinking.

Beware US infiltration

There are always external factors and other unpredictable events which makes forecasting difficult. One of these relates to ‘imported inflation’. This occurs when goods or services are imported from a country that exhibits high inflation. The escalating prices of the imports, whether in the form of manufacturing inputs or finished goods, eventually feed into our CPI figures.

The RBA will be closely watching events unfold in the US which is one of our major trading partners. The US Government’s current spending on stimulus to rebuild US industry has triggered an inflationary response. The annual inflation rate in the US accelerated for a second straight month in March 2024, to 3.5%, compared to 3.2% in February. This is the highest rate since September last year. Also, the US is experiencing the same phenomenon regarding services inflation which increased to 5.27% in March from 4.95% in February of 2024.

Fortunately, inflation in most of Australia’s other major trading partners is subdued. In April 2024, annual inflation in Europe rose by an acceptable 2.4 per cent, unchanged from March. China's inflation rate is even more insipid as consumer prices only edged up a meagre 0.1 per cent for the year to March 2024. Therefore, a watching brief on imported inflation from the US is all that is required at this stage and a knee-jerk reaction should be avoided.

A unified approach

The RBA should be congratulated in carrying out its mission: to get inflation back between the target range of 2 to 3 per cent. We’re almost there. It has exercised wise judgement in pausing any further tightening since November 2023. This strategy allows last year’s rate rises to work their way through the economy. By the same token any premature easing (rate reductions) should be avoided for fear of allowing the inflation genie to escape our realm of control. This is not an exact science and thanks to the recent RBA review, we now have some wise heads around the RBA board table.

Now is the perfect time for the government to step in and lend a hand, like a good teammate. We should remember that monetary policy is not the only tool in our bag. Fiscal policy is also relevant and can often target inflation more precisely in segments of the economy.

This month is crucial as the Albanese government hands down the May budget – a perfect time to exhibit fiscal responsibility. It can start by ensuring that the 1 July tax cuts and ongoing infrastructure pipeline spend are adequately balanced by some contractionary measures. In the process, ensuring it doesn’t cause further harm to the vulnerable, who have been hardest hit in the current cost of living crisis.

A team approach between the government and the RBA sounds like the best way forward, especially at this critical juncture. All going well, the RBA could start its easing program by year’s end and achieve the sub 3 per cent inflation target by 2025. Here’s hoping!

Dr Mazzola is a Lecturer in banking and finance in the School of Business. He has more than 25 years’ banking and finance experience in the Australian, European and Asian Pacific markets. He is the author of Countdown to the Global Financial Crisis: A Story of Power and Greed.

UOW academics exercise academic freedom by providing expert commentary, opinion and analysis on a range of ongoing social issues and current affairs. This expert commentary reflects the views of those individual academics and does not necessarily reflect the views or policy positions of the University of Wollongong.